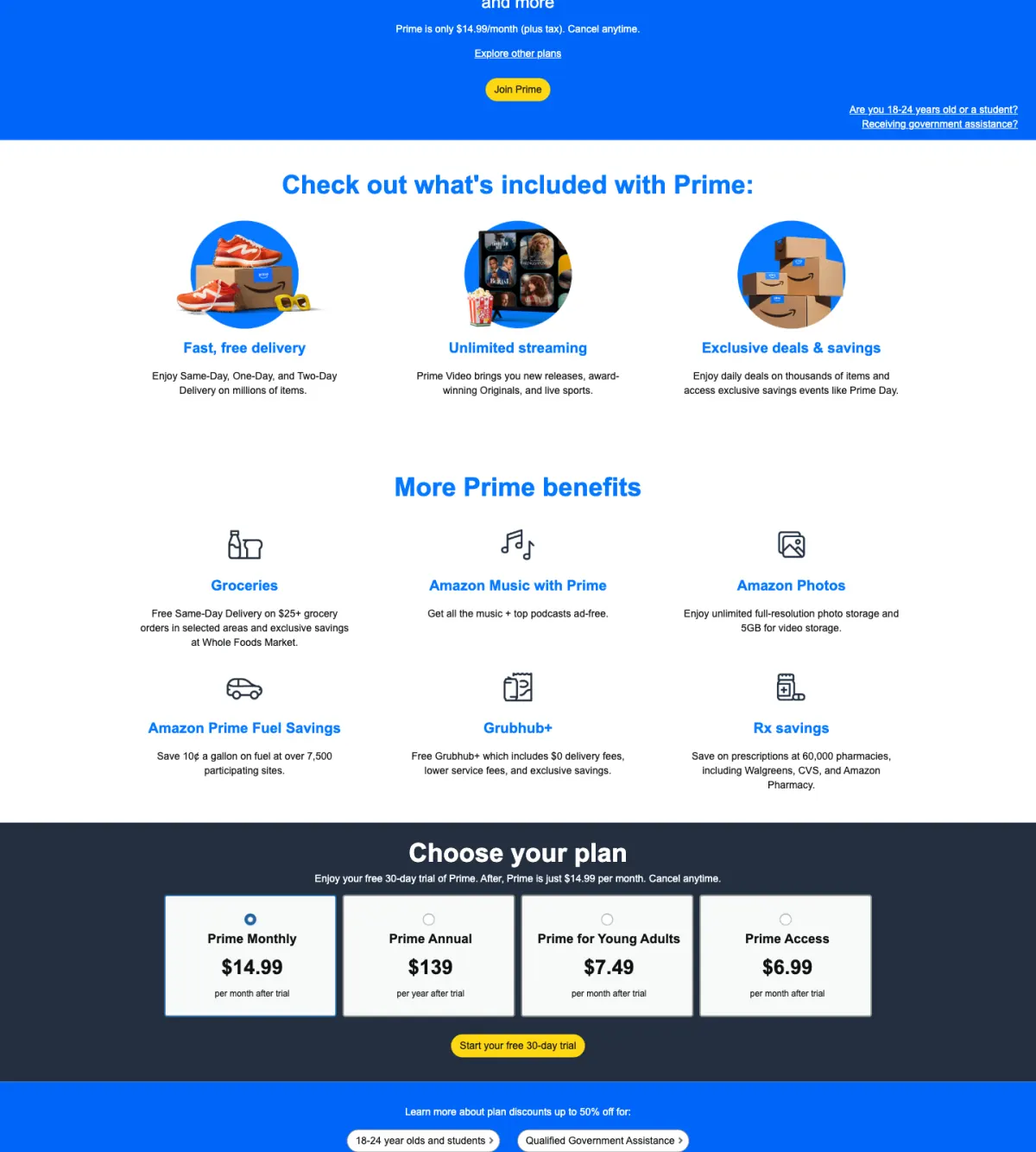

Buying guide✈️ Points & Travel

Best Cards for Amazon Prime and Amazon Spend in 2026

How to maximize rewards on Amazon.com and Whole Foods in 2026 — the 5% Prime Visa rate, why it is really a Prime perk, and the membership math to run before you chase it. Editorial: we link no card applications.

Checked against primary sources, July 2026 · How we verify

We independently score every service with our Experience Index. We may earn a commission if you subscribe through links on this page — it never affects our scores or picks.

The Prime Visa: the 5% that depends on Prime

The Amazon co-brand is the natural anchor for Amazon spend, and its structure is simple. As of July 2026, the Prime Visa earns 5% back at Amazon.com, Whole Foods Market, Amazon Fresh, Audible, and Chase Travel; 2% at gas stations and restaurants and on local transit and rideshare; and 1% on everything else. The annual fee is $0. This is a nominative editorial mention — we link no application here.

The string attached is the one that reframes the whole card: the 5% rate requires an active Amazon Prime membership. As of July 2026, without Prime the same co-brand earns 3% at Amazon rather than 5%. So the marquee rate is not free — it is unlocked by paying for Prime, which means the 5% is best understood as a Prime perk rather than a standalone card benefit.

Without Prime the Amazon card earns 3%, not 5% — so the top rate is effectively something you are paying for through the membership.

Run the membership math first

Because the 5% depends on Prime, the honest first step is pricing Prime itself. As of July 2026, Amazon Prime costs $14.99/month or $139/year, with a Young Adult plan at $69/year for ages 18–24 and Prime Access at $6.99/month for those who qualify. Weigh that against the 2-point gap between the Prime Visa's 5% and a flat 2% card: that gap is worth $2 for every $100 of eligible Amazon spend. To justify Prime on Amazon rewards alone, you would need a large amount of qualifying spend — which is why the membership only makes sense when you value its shipping, video, and other benefits too.

If the membership stands up on its own merits, the Prime Visa's 5% is a genuine bonus on spending you would do anyway. If you are weighing Prime purely for this reward, start with our converter guide, is Amazon Prime worth it?, and if you are trying to trim the add-ons, the best Amazon subscriptions worth it in 2026. You can pick up a membership directly via Amazon Prime once the math checks out.

Matching the card to the purchase

Different Amazon purchases reward differently, and the best move is not always the co-brand. Here is how the common Amazon spend types line up as of July 2026.

| Amazon spend type | Best rate & how |

|---|---|

| Amazon.com | 5% with the Prime Visa (requires active Prime); 3% without Prime |

| Whole Foods Market | 5% with the Prime Visa (requires active Prime) |

| Amazon Fresh | 5% with the Prime Visa (requires active Prime) |

| Audible | 5% with the Prime Visa (requires active Prime) |

| Everything else on Amazon (non-category) | A flat 2% cash-back card beats a card paying only 1%; watch for Amex/Chase Offers credits |

The chart below makes the Prime dependency visual: the same Amazon.com purchase earns three very different rates depending on whether you have Prime and which card you use.

Other routes worth knowing

Beyond the co-brand, two general strategies help, and neither needs a new card application. First, rotating card offers — programs such as Amex Offers and Chase Offers — periodically add Amazon statement credits for enrolled cardholders; they are unpredictable, but free to check and occasionally worth real money. Second, a flat 2% cash-back card is the quiet workhorse for any Amazon spend that does not fall into a 5% category, because 2% comfortably beats the 1% base rate a co-brand or generic card pays outside its bonus categories. Present both as strategy, not as a specific card to go get — this is editorial, and we link no applications.

Who should carry the Prime Visa?

Pros

- You already pay for Prime for its shipping, video, or grocery benefits — the 5% is a bonus on spending you would do anyway.

- You shop Amazon.com, Whole Foods, or Amazon Fresh regularly enough that 5% adds up.

- You want a $0-annual-fee card and are comfortable that the top rate is tied to a membership you already keep.

- You will use a flat 2% card for non-category spend rather than defaulting to a 1% rate.

Cons

- You do not have Prime and would buy it mainly to unlock the 5% — the membership cost can outweigh the reward.

- Your Amazon spend is light, so the 2-point edge over a flat 2% card is small in absolute dollars.

- You dislike managing multiple cards and would rather earn one simple flat rate everywhere.

- You expect 5% on all Amazon purchases — it applies to the named categories, and non-category spend earns less.

Decide the membership question first with is Amazon Prime worth it? and trim the extras with the best Amazon subscriptions worth it in 2026; for the wider view of which cards credit which subscriptions, see the companion inventory, cards that pay for your subscriptions.

Frequently asked questions

What is the best card for Amazon spend in 2026?

Do I need Amazon Prime to get 5% back?

Is chasing 5% at Amazon actually worth it?

Are there other ways to save on Amazon with a card?

Related reading

Is Amazon Prime Worth It in 2026? An Honest Decision Guide

A skeptical look at whether Amazon Prime is worth $14.99/month in 2026 — the full bundle of perks, the "worth it just for shipping?" math, and who should skip it.

12 min read

Are Amazon's Subscriptions Worth It? Prime, Prime Video, Audible & Kindle Unlimited (2026)

One hub to untangle what you actually pay Amazon: Prime bundles Prime Video, but Audible and Kindle Unlimited are separate paid subs. Here's what's included, what isn't, and which are worth it in 2026.

10 min read

Is Prime Video Worth It in 2026? Standalone vs Prime, Ads & Channels

An honest look at whether Prime Video is worth it in 2026 — the $8.99 standalone plan, the ads you now get by default, the new Prime Video Ultra ad-free add-on, and whether you are paying twice with a full Prime membership.

9 min read